Tijana Simic // Shutterstock

The weight loss boom is reshaping American aesthetics

An estimated 63% of weight loss drug patients now seeking facial treatments have never set foot in a cosmetic clinic before.

Thirty-one million Americans are now taking GLP-1 weight loss medications, according to KFF polling data from November 2025.

The weight comes off fast. What many patients do not expect is what it does to their face. The phenomenon has developed a viral name to describe the gaunt, hollowed appearance some patients develop after rapid medication-driven weight loss.

Social media users and news outlets have labeled it “Ozempic face.”

Clinically, it refers to a loss of facial volume in the temples, cheeks, and under-eye area, often accompanied by loose skin and deeper creases.

It has also created an entirely new patient population. RIVKIN Aesthetics, a Los Angeles-based provider of facial cosmetic procedures, traces the data from 31 million prescriptions to a cosmetic industry scrambling to keep up.

The numbers tell the story. McKinsey’s 2025 survey of 174 aesthetics providers found 63% of GLP-1 patients seeking facial treatments had never been active cosmetic medicine users.

Roughly half had never thought about cosmetic work until their weight loss changed the face they saw in the mirror.

GLP-1 drugs are not creating a new demographic. They are turning an enormous existing group, women aged 40 to 64 who already make up the majority of filler patients, into first-time cosmetic clients.

The demand from clinics, the market data, and the search trends all point in the same direction. The cosmetic medicine industry is not being reshaped by changing beauty standards.

It is being reshaped by a class of drugs.

The Scale of the Prescription Surge

Three years. That is how long it took monthly semaglutide prescriptions to grow fivefold, from roughly 472,000 fills in January 2021 to more than 2.5 million by December 2023, per IQVIA data published in JAMA Health Forum.

The broader picture is even more striking. GLP-1 prescriptions for weight loss rose 587% from 2019 to 2024, according to FAIR Health claims data. Among patients using the drugs for weight management rather than diabetes, the increase was 1,961%.

The pharmaceutical industry is scaling to match. Novo Nordisk’s semaglutide portfolio generated approximately $29.3 billion globally in 2024. Eli Lilly’s competing tirzepatide franchise hit $16.4 billion. Goldman Sachs Research projects the global anti-obesity drug market will reach $95 billion by 2030. Morgan Stanley puts it at $150 billion by 2035.

What the Drugs Do to the Face — and What Remains Unknown

The clinical trial data is precise about what leaves the body. In the two largest body composition studies of GLP-1 weight loss drugs, the STEP 1 and SURMOUNT-1 trials, patients lost between 19% and 34% of their total fat mass. Roughly three-quarters of all weight lost was fat. The remaining quarter was lean tissue, including muscle.

But here is the critical gap: No published study has directly measured facial fat loss using imaging in patients on these medications. Every clinical description of the hollowed temples, sunken cheeks, and deepened folds is based on physician observation, not hard data.

What is emerging is more concerning than simple weight loss. A 2024 paper in the Aesthetic Surgery Journal identified GLP-1 receptors on the stem cells that maintain skin health. The drugs appear to inhibit those cells from producing collagen, elastin, and hyaluronic acid, the proteins that keep skin firm and full. A separate lab study confirmed GLP-1 shifts those same stem cells away from producing fat cells entirely.

A 2025 paper in the journal Endocrine put it plainly: the facial aging effect is ‘not exclusively related to decreased facial fat.’ Additional mechanisms have yet to be identified.

The science suggests these drugs may age the face through pathways beyond weight loss alone. The evidence is still early, drawn from lab models rather than clinical trials on human skin.

The demand for treatment, however, is not early at all.

837,000 Patients and Counting

The American Society of Plastic Surgeons reported more than 837,000 GLP-1 patients were seen by its member surgeons in 2024. Of those, 39% were considering surgery and 41% were considering nonsurgical treatment.

Those patients are reshaping clinical practice. The American Academy of Facial Plastic and Reconstructive Surgery documented a 50% increase in facial fat grafting procedures in its 2024 survey, driven largely by weight loss drug patients. Nearly half of facial plastic surgeons reported a noticeable rise in patients citing GLP-1 side effects. One in 10 AAFPRS members have begun personally prescribing GLP-1 medications. They are now on both sides of the equation.

The pattern holds across specialties. A survey of 400 clinicians presented at the American Society for Dermatologic Surgery found unanimous reporting of significant patient increases, with 81% reaching for hyaluronic acid fillers as the first treatment.

The profile of these patients matters. McKinsey’s data shows 61% had lost between 11% and 30% of their body weight. And 63% were not coming in about a single wrinkle or fine line. They were coming in because their whole face had changed.

What It Costs

The financial math is layered. GLP-1 medications themselves run $800 to $1,350 per month at list price, though Novo Nordisk recently lowered its direct-to-consumer price to $349 per month. Medicare’s negotiated price is $245 per month.

Correcting the facial side effects adds a second bill. A single syringe of hyaluronic acid filler averages $684 to $750 nationally, according to ASPS data. Biostimulatory injectables like Sculptra, the type doctors now recommend first for weight-loss patients per a 2025 international consensus study, run $850 to $1,200 per vial. Most patients need multiple vials across multiple sessions.

McKinsey found a telling split. Sixty percent of GLP-1 patients actually reduced their overall cosmetic spending, with drug costs eating into their budgets. But 40% spent more. And the wave of first-time patients represents a customer base the industry never had before.

Where Demand Is Growing Fastest

The geographic story reveals a mismatch that may reshape where cosmetic medicine is practiced in the United States.

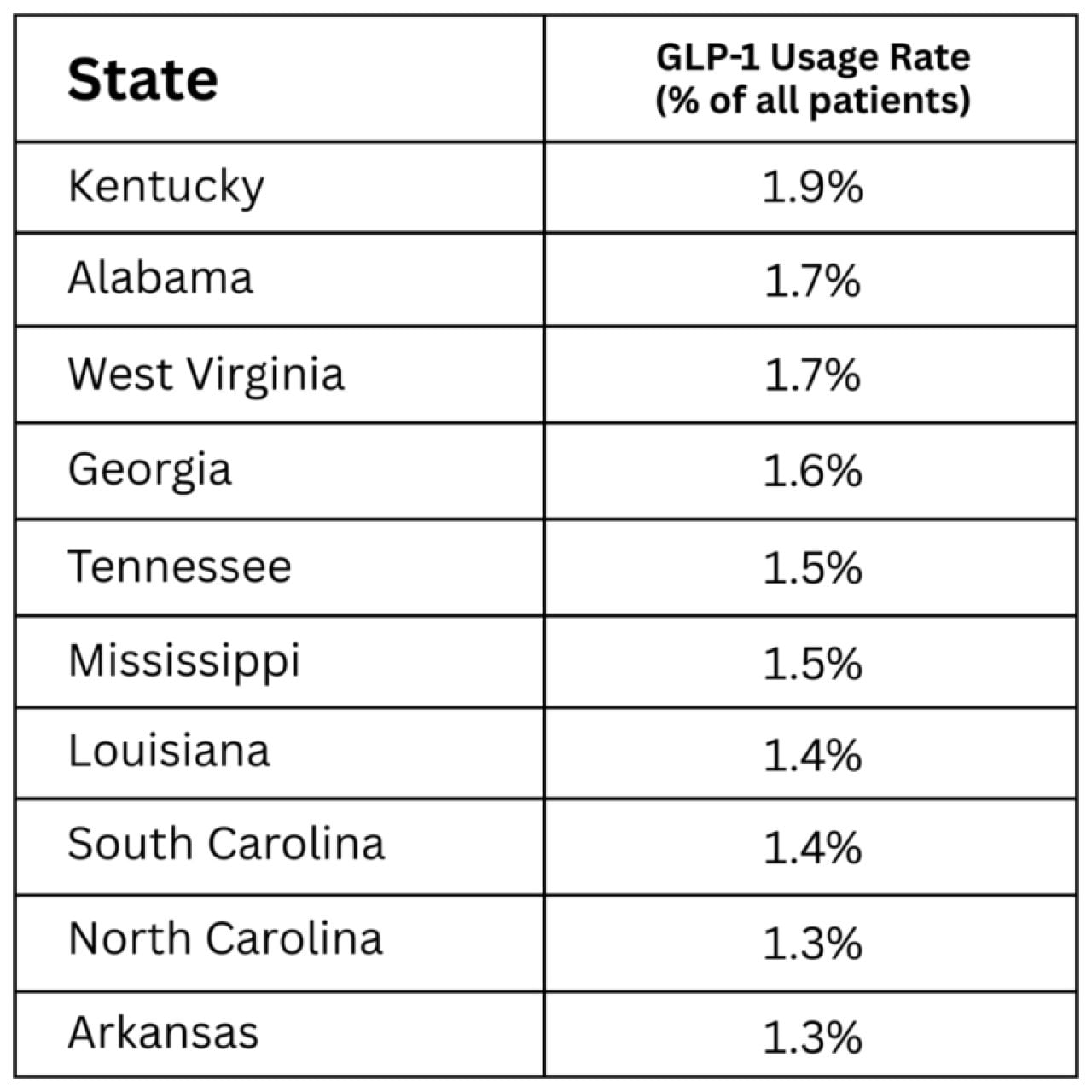

GLP-1 prescriptions concentrate in the Southeast and Midwest, the states with the highest obesity rates. Cosmetic procedure infrastructure concentrates on the coasts. The result: Demand is building fastest where providers are scarcest.

Real Chemistry’s analysis of more than 300 million U.S. patient records shows where GLP-1 usage is highest:

RIVKIN Aesthetics

The lowest rates belong to Hawai’i (0.4%), Arizona (0.5%), and Colorado (0.6%).

The cosmetic industry’s footprint looks nothing like that map. Miami leads the nation with 3.9 plastic surgeons per 100,000 residents. Salt Lake City follows at 3.12. The Mountain and Pacific regions account for more than a third of all cosmetic surgical procedures, per ASPS data.

Google Trends data mirrors the prescription map. The states with the highest search interest in GLP-1 facial side effects are Mississippi, West Virginia, Louisiana, Alabama, and Oklahoma. A 2025 study in PRS-Global Open found those searches directly correlate with rising interest in facial fillers, but not surgical procedures.

Patients are looking for injectable solutions, and many are looking in places where those solutions are hardest to find.

The Industry Response

The U.S. dermal filler market recorded roughly 6.26 million procedures in 2024, according to ASPS data. That total has doubled since 2017. But the growth is shifting beneath the surface.

Traditional hyaluronic acid filler growth slowed to 1% year-over-year in 2024. The category gaining ground is biostimulatory fillers, products like Sculptra that trigger the body’s own collagen production rather than simply adding volume. Galderma reported double-digit global growth for Sculptra in 2024. Qsight market tracking data confirms biostimulators are now carrying the broader filler market while traditional fillers flatten out.

New entrants are betting on GLP-1 patients specifically. Evolus received FDA approval for its first hyaluronic acid fillers in February 2025, citing weight loss drug demand directly in its marketing. The med spa sector has grown to over $17 billion, according to the American Med Spa Association. The number of U.S. med spas jumped from 8,899 in 2022 to 10,488 in 2023, a 15.2% increase in a single year.

KFF data suggests the wave has not crested. Usage among adults aged 50 to 64, the age group most likely to see visible facial changes and most likely to seek treatment, stands at 22% and rising. Drug prices are dropping. Insurance coverage is expanding. The pool of patients is getting larger, and the faces looking back at them in the mirror are getting thinner.

Methodology

GLP-1 prescription data was sourced from the IQVIA National Prescription Audit (as reported in JAMA Health Forum), the ClinCalc DrugStats Database (Medical Expenditure Panel Survey), the CDC’s National Health Interview Survey (NCHS Data Brief No. 537), FAIR Health claims data, KFF Health Tracking Polls, and RAND American Life Panel surveys. Procedure volume data was sourced from the American Society of Plastic Surgeons 2024 Procedural Statistics report and the AAFPRS 2024 annual survey. Clinical evidence was drawn from the STEP 1 body composition substudy (Journal of the Endocrine Society), the SURMOUNT-1 substudy (Diabetes, Obesity and Metabolism), and mechanistic studies in the Aesthetic Surgery Journal (2024) and Endocrine (2025).

Market data was sourced from company earnings reports (Novo Nordisk, Eli Lilly, Galderma), McKinsey & Company’s 2025 survey of aesthetics providers, Goldman Sachs Research, Morgan Stanley Research, and the American Med Spa Association 2024 State of the Industry Report. Geographic data was sourced from Real Chemistry’s IRIS platform analysis of over 300 million U.S. patient records. Search trend data was sourced from peer-reviewed analyses in the Journal of Cosmetic Dermatology (2026), PRS-Global Open (2025), and the Aesthetic Surgery Journal (2024). All data represents the most recent publicly available reporting as of February 2026.

This story was produced by RIVKIN Aesthetics and reviewed and distributed by Stacker.

![]()